Digital is redefining everyday lives. Our life experiences are shaped by digital forces. The artificial intelligence and internet of everything are on the cusp of becoming a daily reality. However, the financial and economic transactions in our digital lives are still ruled by old paradigms. The need for a third-party intermediary to verify our identity and intent still exists. It creates a slow, old, vulnerable and expensive system which has been the basis of our financial world. Blockchain aims to redefine this antiquated system.

Blockchain is the breakthrough technology that is revolutionizing the world economy. It is essentially an open-source distributed database. The digital database uses state-of-the-art cryptography and mass collaboration to authenticate and settle transactions. The ever-expanding chain of computers form the network and everyone on the networks approves an exchange before it is verified and recorded. It is truly open source, peer-to-peer and highly secure – thus becoming the platform of trust.

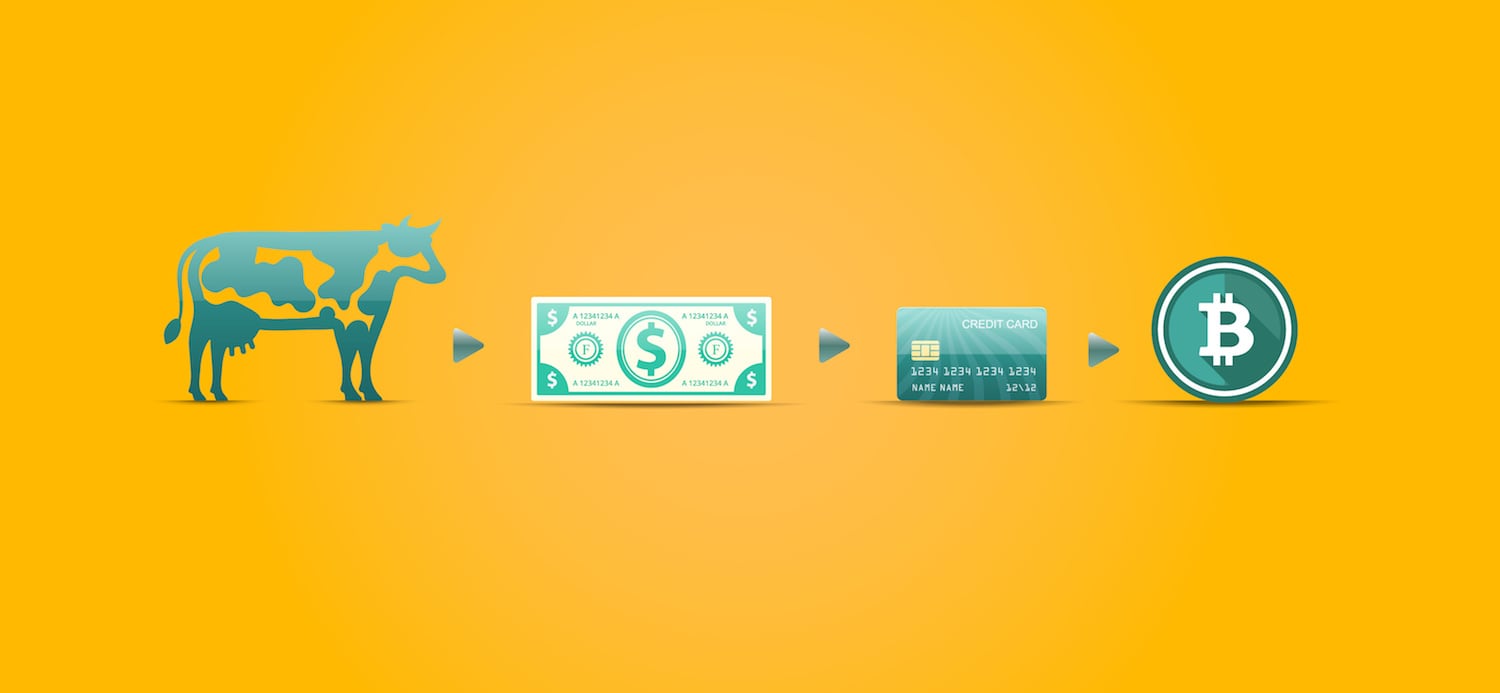

Bitcoin was the first use case of Blockchain. The power and potential of Blockchain lies in its ability to represent anything digital – rights, goods and property. The emerging use cases of Blockchain include:

1. Property Rights / Land Records – Governments can avoid fraudulent deeds, manipulation of records and conflict of ownership by leveraging Blockchain

2. Electronic Medical Records – Healthcare industry has multiple stakeholders accessing patient information. Hospitals, doctors, insurance companies, governments etc. can be confident that they are working on secure, encrypted and genuine records using Blockchain

3. Certificate of Authentication – Fraudulent transactions will be avoided as every transaction is recorded and distributed on public ledger.

4. Certification of Compliances – Everledger has authenticated more than 1000,000 diamonds using Blockchain. It has developed a system of warranties that enable mining companies to verify that their rough-cut diamonds are not being used by militias to fund conflicts. Thus, it ensures compliance with Kimberley Process. Bye Bye Blood Diamonds.

5. Share Ownership Registry – US Securities and Exchange Commission (SEC) has approved the use of the Blockchain as a share ownership register for online retailer Overstock.com.

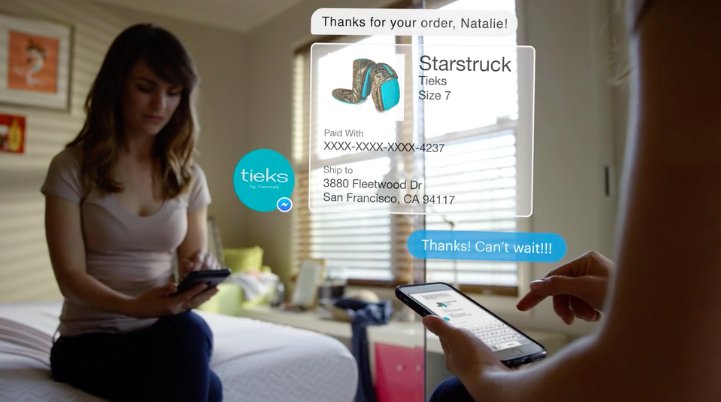

6. Micropayments: People wanting to read just one article or subscribe to 2 channels on Cable TV can use the Blockchain Infrastructure. ChangeCoin allows instant transfer of value irrespective of size. Similarly, Chain allows to give tip to a blogger or car share driver – very useful in a sharing economy.

7. Data Privacy – Estonia, the leading European country in digital services uses a Blockchain implementation to manage and protect its citizens’ data across about 1,000 online services.

8. Patents & Innovation – Authentication and verification

9. ESOPs for Employees

10. Wills

11. Tax Collection

12. Remittance of Funds to Unbanked

It is not surprising that all the leading companies in the world are working on Blockchain in some form or the other. Microsoft has built multiple offerings on Blockchain by leveraging its Azure platform. IBM, PWC, UBS, Bank of Canada are other organizations working on Blockchain. Who’s Who have joined Hyperledger – including Amex, Wells Fargo, J P Morgan, Intel, IBM, BNP Paribas, Samsung, Intuit etc. R3 is leading a consortium of 75 world’s leading financial institutions including Wells Fargo, Barclays, UBS to design and deliver advanced distributed ledger technologies. Billions of dollars are being invested in Silicon Valley startups working on Blockchain.

Several institutions including financial organizations will be severely impacted by Blockchain as it bypasses the traditional channels. Governments, legal agencies, enforcement organizations will need to understand and embrace this technology. Often the ignorance of the potential of Blockchain and understanding of its working causes skepticism about the technology. Blockchain enthusiasts need to educate, inform and demonstrate the benefits in action.

The rise of Blockchain is imminent. The speed of the rise will be determined by social, legal, political and human acceptance.

Image Credit: Blockchaintechnologies.com